How TRIZ Can Help Fix the Global Crop Insurance Crisis

Why Crop Insurance Keeps Failing and What Systematic Innovation Design Tells Us About Fixing It

Crop insurance is one of those problems that never quite gets solved. Year after year, billions of Euros flow into subsidies, pilot programs, and redesigned products; Yet the global agricultural insurance protection gap keeps widening. Farmers in drought-prone regions remain unprotected. Insurers struggle with solvency. Governments keep absorbing losses they cannot afford.

The question worth asking is not “why isn’t there enough funding?”, there is often plenty of that. The real question is: why does the structure of crop insurance itself keep producing the same failures, regardless of how much money gets thrown at it?

This is where an unlikely tool becomes surprisingly useful: TRIZ, the Theory of Inventive Problem Solving. Originally developed in the Soviet Union for engineering breakthroughs, TRIZ is a systematic framework for identifying and resolving structural contradictions inside complex systems. And crop insurance, it turns out, is full of them.

At Zetarium, we build parametric insurance tools grounded in exactly this kind of systems thinking, the belief that better agricultural insurance starts with better system design, not just bigger budgets. This article lays out why that matters and what a redesigned crop insurance architecture could look like.

What Is TRIZ, and Why Does It Matter for Agricultural Finance?

TRIZ was created by Soviet engineer and inventor Genrich Altshuller in the late 1940s. After spending years in a Siberian prison camp, Altshuller returned to a singular question: Is there a systematic method for invention, or does every breakthrough rely on luck? His answer, built from the analysis of hundreds of thousands of patents across dozens of industries, was a resounding yes.

What Altshuller found was this: breakthrough inventions are not random. They repeatedly resolve the same types of structural contradictions. A problem that looks unique in aviation often shares its underlying logic with a problem in manufacturing, medicine, or logistics. TRIZ identifies those patterns and turns them into reusable problem-solving tools.

The core toolkit includes:

- Contradiction matrices: to identify which inventive principles apply to a specific conflict

- Separation principles: to resolve contradictions by separating conflicting requirements in time, space, or condition

- Substance-field models: to map how elements of a system interact and where they break down

- The concept of the Ideal Final Result: defining what a perfect solution would look like before designing toward it

TRIZ has been applied widely in engineering, manufacturing, software design, and logistics. More recently, it has found serious application in financial system design, and crop insurance is one of the clearest cases where it belongs.

Why Crop Insurance Is Structurally Broken, Not Just Underfunded

It is tempting to frame the crop insurance crisis as a resource problem. Developing countries lack sufficient capital. Governments underfund subsidy programs. Reinsurers price catastrophe risk too conservatively for frontier markets. All of that is true, but it describes symptoms, not the underlying design flaw.

Agriculture faces a category of risk that is genuinely hostile to conventional insurance logic:

- Drought and flood damage thousands of farms across an entire region simultaneously

- Climate volatility makes historical actuarial data less and less reliable as a pricing basis

- Pest and disease outbreaks spread across geographies faster than claims can be assessed

- Extreme heat events can wipe out an entire growing season in weeks

None of this is new. But it creates a structural problem that traditional insurance was never designed to handle.

Traditional insurance works by pooling independent risks. If ten thousand people each face a small, independent probability of loss, the law of large numbers makes the pool manageable. Agricultural climate risk violates that assumption. When a drought hits, it hits everyone in a region at once. The losses are correlated, not independent. And as climate volatility increases, the correlations get stronger.

This is not a problem you can solve by adding more policyholders or raising premiums. It is an architectural problem, and that is precisely what TRIZ is designed to address. For a detailed look at how this plays out in agricultural finance more broadly, see our article on the current state of agricultural financing.

The Core Contradiction: Affordability vs. Solvency

TRIZ always begins with the same question: what is the core contradiction inside the system?

In crop insurance, it is painfully clear:

Premiums must stay low enough that farmers can afford to participate, and high enough that insurers remain solvent when catastrophic losses arrive.

You cannot satisfy both requirements at the same time within a conventional insurance structure. Every attempt to do so ends in the same place: either farmers can’t afford the product, or insurers can’t survive a bad year without a government bailout.

The standard responses (premium subsidies, public-private partnerships, microinsurance programs) are all forms of compromise. They shift the cost; they don’t resolve the contradiction. TRIZ argues that compromise is rarely the answer. The goal is to separate the contradictory requirements so that each can be fully satisfied on its own terms.

To frame this formally in TRIZ language, the technical contradiction looks like this:

| Improve | Worsens |

| #26 — Quantity of Substance (scale of insured farmers, premium volume, capital pool size) | #27 — Reliability (solvency under correlated, catastrophic climate losses) |

Increasing pool size improves affordability and efficiency, but simultaneously increases aggregate exposure to the exact catastrophic events that could destroy solvency. The system gets stronger on one axis and more fragile on the other.

TRIZ resolves this not by seeking a middle ground, but by redesigning the system so the two requirements no longer conflict.

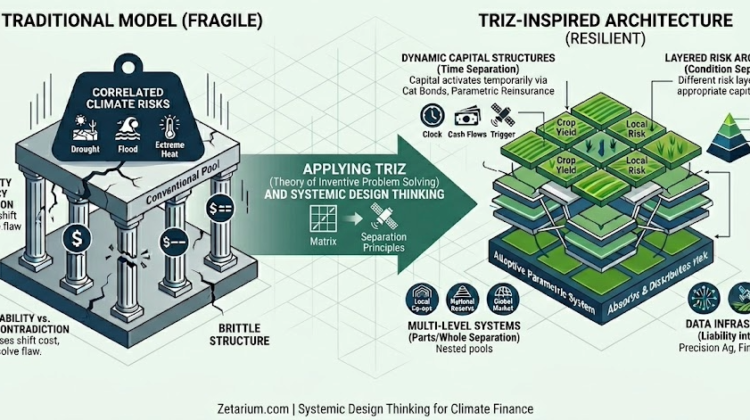

Applying TRIZ: Four Structural Solutions for Crop Insurance

The TRIZ contradiction matrix, applied to the parameters above, points toward several inventive principles with direct relevance to agricultural insurance design. When we treat the problem as a physical contradiction (the system simultaneously needs low and high premiums), TRIZ offers four separation strategies.

1. Separation in Time: Dynamic Capital Structures

The first insight is straightforward once you see it: premiums do not need to be high all the time. They only need to be high when catastrophic risk materializes.

During normal seasons, premiums stay affordable, participation expands, and routine claims are handled conventionally. When a systemic climate event strikes, external capital activates temporarily, not from insurer reserves, but from dedicated financial instruments designed for exactly this purpose:

- Catastrophe bonds that trigger automatically at predefined weather thresholds

- Parametric reinsurance that pays out based on satellite-measured conditions rather than individual loss assessments

- Contingent credit facilities pre-arranged with development banks

- Sovereign emergency mechanisms for national-scale events

This transforms agricultural insurance from a static reserve model (where the money must always be sitting in a capital buffer) into a dynamic capital-access model. The capital exists in the financial system; it just activates when needed.

The TRIZ principles at work here are:

- Principle 10 (Preliminary Action): catastrophe financing is arranged before a disaster, not scrambled for during one

- Principle 15 (Dynamics): the insurance system adapts continuously to changing climate conditions, rather than fixing parameters in advance

- Principle 35 (Parameter Changes): premiums, deductibles, and reserve requirements adjust in real time based on current risk indicators

2. Separation Upon Condition: Layered Risk Architecture

The second insight is that not all agricultural losses are the same, and they should not be financed the same way.

A small crop loss from localized hail is a different kind of event than a national-scale drought. Treating them identically inside one premium structure is precisely what creates the affordability-solvency contradiction. TRIZ resolves this through segmentation: different risk layers, different capital sources, different pricing logic.

A well-designed agricultural insurance structure might look like this:

| Risk Layer | Capital Source |

| Small, frequent losses | Farmer deductible |

| Moderate regional losses | Commercial insurers |

| Severe correlated losses | Reinsurance markets |

| Extreme systemic catastrophe | Catastrophe bonds, sovereign facilities, and development banks |

This layered structure removes the pressure to make a single premium mechanism do everything at once. Routine losses are affordable because they are handled at the farmer level. Catastrophic losses are manageable because capital is pre-positioned at the right level of the financial system.

Relevant TRIZ principles here include Principle 1 (Segmentation), Principle 3 (Local Quality, differentiating risk pools by geography, crop type, climate exposure, and irrigation access), and Principle 40 (Composite Structures, combining multiple financing mechanisms into one integrated capital architecture).

3. Separation Between Parts and Whole: Multi-Level Insurance Systems

A local insurance cooperative in rural Zambia does not need to independently survive a continent-wide drought. Expecting it to do so is a design error, not a funding gap.

TRIZ resolves this by separating where affordability operates from where solvency operates. Local pools remain:

- Small enough to be administratively lightweight

- Specialized enough to reflect local crop conditions

- Affordable because they only absorb local, manageable losses

System-wide solvency, on the other hand, emerges from interconnected national and global structures:

- National reserve systems and agricultural development banks

- Global reinsurance markets that distribute risk internationally

- Climate-linked securities that bring capital-market investors into agricultural risk

- Multilateral institutions like the World Bank’s agriculture finance arms

This is TRIZ Principle 7 (Nested Doll) in action: small insurance structures exist inside progressively larger protective layers, each with its own function and funding logic. The relevant TRIZ principles are also Principle 24 (Intermediary: external institutions absorb systemic volatility) and Principle 40 (Composite Structures: resilience emerges from interconnected layers).

4. Turning the Liability into an Asset: Agricultural Data Infrastructure

Perhaps the most counterintuitive insight TRIZ offers here comes from Principle 22: Blessing in Disguise. The very scale that creates catastrophic liability also generates something enormously valuable: data.

A large-scale agricultural insurance system running across thousands of farms and multiple growing seasons produces:

- Detailed yield histories correlated with weather and soil conditions

- Climate-response patterns specific to crop varieties and farming practices

- Satellite-linked production intelligence at the field level

- Carbon accounting infrastructure valuable to voluntary carbon markets

- Soil productivity analytics that no other industry is systematically collecting

These datasets have value far beyond insurance. They can directly support agricultural credit underwriting, supply-chain finance, precision agriculture technology, commodity price forecasting, and carbon market verification. In other words, the liability side of the scale can partially fund itself through the informational assets it generates.

As we explored in our piece on de-risking agribusiness finance, data is increasingly the foundation of durable agricultural risk management.

What This Means for Insurers, Investors, and AgTech Firms

If you work in agricultural insurance, reinsurance, agricultural lending, or AgTech, the TRIZ analysis above has direct implications for how you should think about the market’s evolution.

For Insurers

Traditional actuarial models are going to become increasingly unreliable as climate patterns shift. The insurers who survive will not be those with the largest capital buffers; they will be those with the most adaptive underwriting systems. Real-time satellite data, parametric triggers, and layered reinsurance structures are not optional upgrades; they are the future architecture of solvency.

For Investors

Agricultural climate risk is becoming an investable asset class. Catastrophe bonds, climate-linked securities, and agricultural data infrastructure represent genuinely new categories of financial instruments. The organizations structuring these products are not conventional insurers. They look more like data platforms with financial products attached.

For AgTech Firms

If your platform generates field-level agricultural data, you are sitting on solvency infrastructure, whether or not you currently think of it that way. Yield histories, soil indices, and satellite monitoring outputs are exactly what the next generation of crop insurance architecture needs. The relationship between AgTech and insurance is going to get much tighter, and the firms that position themselves at that intersection early will define the category.

The transition underway in agricultural credit reflects the same dynamic; for context, read our article on the new architecture of agricultural credit.

Conclusion: The Crop Insurance Crisis Is a Design Problem, Solution TRIZ

The global crop insurance crisis is usually described as a funding problem. TRIZ reveals something more precise: it is a system design problem, and funding alone cannot solve it.

The conventional structure of agricultural insurance was built for risks that are independent, statistically stable, and geographically diversifiable. Climate-linked agricultural risk violates all three assumptions simultaneously, and as climate volatility increases, the gap between the system’s assumptions and reality will only widen.

The path forward is not to simply expand subsidies or enlarge existing insurance pools. It is to redesign the system architecture itself: separating contradictory requirements across time, condition, and organizational scale; pre-positioning capital through dynamic financial instruments; differentiating risk layers with appropriate capital sources; and converting the liability of scale into the asset of data.

Related External References